Ours is an age of rapidly ageing societies. What is so modern about our current situation is not the ageing itself, but its velocity, and its global extension. West European societies have been ageing steadily – in terms of their median population age - ever since the coming of the industrial revolution, but now, following a sharp fall in birth rates and a sustained rise in life expectancy, we are ageing far more quickly than any previous generation could have contemplated. Median ages in several countries are now around the 45 mark, and by 2030 the first pioneers will be breaking the 50 year barrier,

The economic and social implications of this are going to be profound, and, as the credit rating agency Standard & Poors noted in a recent report on the topic, seemingly irreversible. Indeed, no other single force is likely to shape the future of national economic health, public finances, and policymaking in the coming decade as the unprecedented rate at which the world's population is ageing, and the fact that the process is seemingly irreversible. Yet, strangely, the issue receives only a fraction of the attention that has been devoted to global climate change, even though, arguably, ageing is a problem our social and political systems are, in principle, much better equipped to deal with.

Among demographers, and economists interested in demography, the problem has been long been a source of anxiety, and a cause for preoccupation, and as a result a good deal of research which can help us understand and anticipate events has already been carried out, even if policymakers have, to date, been reluctant to act on findings or draw the necessary conclusions.

The problem is, potentially, massive. According U.N. data, the proportion of the world's population aged over 65 is set to more than double by 2050, rising to 16.2% from 7.6% currently. By the middle of the century, about 1 billion over 65s will join the ranks of those currently classed as being of non-working age. The cost of supporting and caring for all these people will inevitably profoundly affect economic growth prospects and dominate public finance policy debates worldwide for many years to come.

As far as we are able to understand the issue at this point, population ageing will have major economic impacts and these can be categorised under four main headings:

i) ageing will affect the size of the working age population, and with this the level of trend economic growth in one country after another

ii) ageing will affect patterns of national saving and borrowing, and with these the directions and magnitudes of global capital flows

iii) through the saving and borrowing path the process can influence values of key assets like housing and equities

iv) through changes in the dependency ratio, ageing will influence pressure on global sovereign debt, producing significant changes in ranking as between developed and emerging economies.

As can be seen, the consequences are far reaching, and will serve as a challenge to our current models of economic growth, and consequently to our existing welfare systems for many years to come. Many of the issues involved – global economic imbalances, sovereign debt worries, the raising of retirement ages – are far from being unfamiliar topics in the context of the present financial crisis, as they have, one after another, come to the forefront. And it is here the greatest concern lies: given the difficult and protracted exit from the last global crisis, may we in fact find ourselves in the unfortunate position of saying goodbye to one crisis only to find ourselves saying hello to another, the ageing population one?

Structural and Numerical Change In the Labour Force

The problem of population ageing is universal, as it is triggered by the decline in fertility that accompanies economic development, and will affect all the nations on the globe one day or another. The short term impact of population ageing, however, will be much more localised, since the pace of aging varies greatly across countries and regions. The effects of the process are expected to be most pronounced in those countries that remained complacent in the face of ultra-low fertility rates (those with total fertility rates of 1.5 and under), which in effect means Japan, the German speaking countries and much of Southern and Eastern Europe. It is estimated that the median age of populations in Europe as a whole will increase from 38 today to 49 in 2050 (although this aggregate number hides significant differences between countries), and by that time Europe will be some 20 years older than the estimated average for Africa (which will be the youngest continent).

Spain - with half its population older than 55 by 2050 – is expected to become the oldest country in the world, followed closely by Italy and Austria, with a projected median age of 54. These numbers are very high, and command respect, especially given the notable structural changes we have already seen in the German and Japanese economies, even though these countries have still only median age landmark of 45.

Another way of looking at such demographic changes is in terms of the dependency ratio,

which can be defined in a number of different ways depending on the problem being addressed. One of the most common practices is to take the overall demographic

dependency ratio, which is conventionally defined as the ratio of the “dependent” age

groups (0-14 and 65+) to the population in what have been traditionally considered to be the working age groups (15-64). Both the sub-components to the overall ratio are expected to change significantly over the next 50 years, with the important detail that they will move in opposite directions, with ever fewer young people, and ever larger elderly populations, although it is the second component – the elderly dependency ratio - which is the principal centre of interest in the present study.

During the years belween 1960-1995 the overall dependency ratio fell across the developed world, with decreases in the proportion of young people more than offsetting the rise in the old age dependency ratio, and working age populations rising everywhere. These were the years of economic bonanza, economic growth and exceptional returns in the property, fixed income and equity markets.

Since the mid 1990s the situation has been gradually changing, and the overall dependency ratio is now rising steadily again, this time thanks to the increase in life expectancy, and smaller generations entering the workforce as a result of the substantial long term drop in fertility. The ratio is forecast to increase over the next 40 years by a “mere” 15 percentage points in the United States, and by as much as 22 and 40 percentage points in the EU and Japan respectively. If we consider the elderly dependency ratio alone, in 1985 the EU ratio of over 65s to those between 15-64 was 20% i.e. there were five potential workers for every one retired person. By 2050 that ratio is expected to deteriorate dramatically to only about two economically active workers for every person over 65.

In terms of the velocity of change, Japan’s situation seems is clearly the most problematic in the short term, since the country is set to experience the steepest climb in dependency ratios roughly 10-15 years before the EU and the US. Of course, it is important to note that Japan has already started to react to the problem, and labour force participation rates among males in the 70 to 75 age range in Japan are currently not dis-similar to those to be found among males in the 63 to 65 age group in many European societies.

It is important to realise that in most cases not only will populations get older, they also will actually shrink. Aside from extreme situations like the black death or major wars, Western societies have no real experience of dealing with ongoing population ageing and sharp population decline.

In Germany, for example, the total population is expected to fall from its current level of 82 million reaching anything between 69 and 74 million by 2050, depending on the future course of life expectancy, immigration and fertility. And the proportion of people aged 65 and older is projected to rise from just under 20% today to just over 33% by 2050. At the same time, the number of very elderly (those aged 80 and over) will nearly triple to as much as 15% of the total population.

Future population developments in Spain involve a greater than normal level of uncertainty at the present time due to the very rapid population increase produced by immigration during the first decade of the century. Migration not only increases population size directly, but also indirectly, due to a higher level of births which results from the sudden increase in those of child bearing age. Bearing this in mind, the INE currently estimate that Spain’s population should continue to grow, and increase by something like 2.1 million over the next 40 years with the country having a population of approximately 48 million in 2049. It should be emphasied though that this increase is dependent on continuing inward migration, and therefore, since the majority of migrants reaching the country are economic migrants, their arrival is very sensitive to the actual levels of GDP growth attained.

As elsewhere, Spain’s elderly population will continue to grow, both in relative and absolute terms, and the population of 65 and over looks set to double in size, coming to represent almost 32% of the total population on the INE estimate, while the working age population is expected to fall by nearly a fifth. The result will be that for every 10 persons of working age, by 2050 there are expected to be almost nine potentially inactive persons (either under 16 years or over 64). That is, the dependency rate is set to rise to 89.6%, from its current 47.8%. Life expectancy at birth is expected to reach 84.3 in males and 89.9 in females by 2050, meaning there could well be an increase of something like 6.5 and 5.8 years, respectively, from their 2007 levels.

Among emerging economies, the East of Europe stands out as by far the worst case in the short term. In 2025, more than one in five Bulgarians will be over 65 - up from just 13 percent in 1990. Ukraine’s population will shrink by a fifth between 2000 and 2025. And the average Slovene will be 47.4 years old in 2025 – one of the oldest populations in the world. Indeed, between 2000 and 2005, the only countries in the world with population declines of more than 5,000 people were 16 countries in Eastern Europe and the former Soviet Union - led by the Russian Federation, Ukraine, Romania, Belarus, and Bulgaria. So the fastest aging countries on the planet over the next two decades will be in those of Eastern Europe and the former Soviet Union, the result of unprecedented declines in fertility and rising life expectancies. The entire region (excluding Turkey) is projected to see its total population shrink by about 23.5 million, with the largest absolute declines taking place in Russia, followed by Ukraine and Romania.

Indeed, the impact of the population decline will be much larger in some of the smaller countries, which will lose a significant share of their populations over the next two decades. Latvia (2.3 million people) and Lithuania (3.4 million) will lose more than a tenth of their population. Poland will lose 1.6 million, or about 4 percent of its 38 million people.

And in the East as elsewhere the impact of the changes will pricipally be felt through

the rising proportion of the elderly people. Most countries had old-age shares (defined as the percentage of the population older than 65) of less than 15 percent in 2000, but this benchmark will be exceeded by almost all of them come 2025 with the largest increases (8 percent or more) being expected to occur in countries that already have older populations, such as the Czech Republic, Poland, and Slovenia. Bosnia and Herzegovina will see the fastest increase, with its elderly dependency ratio almost doubling. For nine countries, between one fifth and one quarter of the population will be 65 and older by 2025 - comparable to the situation in Italy, where the proportion is projected to be about 26 percent. even further increases, to as high as 47 years in the Czech Republic and Slovenia, approaching Italy’s median of 50 years.

And the problem goes well beyond the confines of the EU or the G7. If our experience to date is anything to go by, all societies will experience a similar ageing process as they develop. In particular China stands out among developing economies, since the degree of ageing we should anticipate, when viewed in terms of absolute numbers and velocity, is simply staggering. By 2040, assuming current demographic trends continue, there will be 397 million Chinese over 65 - more than the total current population of France, Germany, Italy, Japan, and the United Kingdom combined. While the forces behind China’s ultra rapid demographic transformation - falling fertility and rising longevity - are similar to those to be found elsewhere, China’s ageing is characterised by the unusual speed with which it is occuring. In Europe, the population over 65 passed the 10 percent threshold back in the 1930s and will not reach the 30 percent mark until the 2030s, one century later. China, on the other hand, will traverse this same distance in a single generation.

And the scale of the Chinese phenomenon should alert us to another looming problem. Up to now, Western societies have managed to slow their ageing rate down, and smooth the transformation of their population pyramids, by resorting to immigration to fill the gaps in the labour force. China’s labour force growth has been driven in recent years, as it was in the Spain of the 1960s and 70s, by internal migration. But now that process is coming to an end, and with the working age population now about to peak, labour supply may well (incredible as it may seem) start to become a scarce factor, and since immigration on any meaningful scale is not a realistic alternative for China, wages are bound to rise, and the economy is bound to become more capital intensive.

With its extra large baby boom cohorts now in its thirties and forties, the full force of China’s ageing challenge still lies out in the future, and the elder share of China’s population has risen only modestly to around 12 percent, compared with an average of 20 percent in the developed countries. For the time being, the big challenge is finding jobs for China’s large working-age population. It is during the 2020’s that China’s age wave will arrive in full force. The elder share of China’s population seems set to rise steadily from 11 percent in 2004 to 15 percent in 2015, and then leap to 24 percent in 2030 and 28 percent in 2040. Over the same period, China’s median age will climb from 32 to 44. A median age of 44 will not make China the oldest country in the world. Germany’s median age is already 45 and is heading for 50 by 2040. Japan’s is already 45 and is heading for 54. A median age of 44, however, will make China an older country than the United States.

Evidently, with these sharp declines in working age populations, rates of economic growth are sure to decline, and may even turn negative. The only factors which can conceivably offset the decline are changes in participation rates, and increased productivity, but with the median age of the workforce rising, and higher participation rates implying an lower average rate of educational qualifications, even measures which lengthen the working life are unlikely to be fully able to extend the impact, and we may well be facing a decline in living standards in the OECD countries in the years to come, especially when compared with the rapid growth and youthful workforces which will be found in many parts of the developing world.

Saving and Borrowing Across The Life Cycle

Crucial to any analysis of the likely economic consequences of population ageing is the impact the process will have on patterns of saving and borrowing. The motives which influence the levels of household saving have been the topic of much debate over the decades, and a variety of explanations have been put forward in the theoretical literature. Essentially the interpretations can be grouped together under three headings with, as one would intuitively expect, assumptions about the time horizon over which the individual takes decisions being one of the key factors which sets one competing hypothesis apart from the next.

The life cycle model of Franco Modigliani (Modigliani and Brumberg, 1954), which is perhaps the most widely accepted version of the saving and borrowing story, assumes the relevant time horizon to be the lifetime of the individual, arguing that what the individual attempts to do is maximise his or her own consumption. In this model, the desire to smooth one’s lifetime consumption path by evening-out cyclical income fluctuations provides the fundamental driving force behind saving/dissavings decisions during different periods, with the need to provide sufficient resources for retirement being the clearest example of such life-cycle effects.

Normally, those working with life-cycle hypothesis models assume a lifetime planning horizon for the individual consumer, with no net lifetime savings being envisaged and transfers to heirs being treated as equivalent to the individual’s own initial inheritance. Leave the world as you found it seems to be the maxim guiding the individual.

The principal modification to the initial life cycel idea – the bequest or “overlapping generations” model - assumes that the individual’s time horizon is multigenerational with strong ties linking current generations to their descendants and with individuals driven to maximize not only their own utility but also that of future generations through a bequest motive. Unlike the “finite” life cycle consumers therefore, their more “Ricardian” counterparts are assumed to have “infinite” lives in the sense of having strong links to their descendants via the above mentioned bequest motive. Leave the world as you would like to have found it seems to be the maxim here.

Finally, the precautionary or “buffer stock” theory of saving is built on the view that a major motive for holding and accumulating assets is to shield one’s consumption against future uncertainties, such as unpredictable fluctuations or disruptions in income or extraordinary health expenditures. One of the intuitive implications of this “buffer stock” model is that individuals with higher income uncertainty should amass a greater stock of wealth to allow for this, and obviously those entering the later stages of their lives face more potential uncertainty than most, and in this sense the implications of the model for our current concerns are not that different from those of the Modigliani model.

When it comes to the empirical modelling of consumer behaviour, and especially in the larger multinational models, some variant of the permanent income/life cycle approach (PIH/LCH) is typically applied, with virtually all mainstream models emphasising the importance of forward looking consumers and consumption smoothing as a way of managing significant changes in their incomestream . The success of the PIH/LCH approach has been based not only on the clear compatability with standard microeconomic utility maximising theory but also on its empirical explanatory power since the predicted outcomes are reasonably compatible with the available evidence both in the the short and long run. Over the long run, the hypothesis suggests that wealth (i.e. permanent income) is the main factor determining consumption with the key consumption-to-wealth ratio being a relatively stable one. In the short-run the PIH/LCH approach is reasonably compatible with Keynesian attitudes to demand management, since it helps explain why consumption fluctuates less than disposable income over the business cycle, due to the presence of consumption smoothing by consumers.

On the other hand the LCH framework is not without its problems, and some of these are important for our present purposes. In particular the savings behaviour of retired people turns out to be very different what might be expected given a simple application of the LCH model. Ageing populations, for example, would be expected to show a lowering of the private savings ratio if the savings pattern of consumers was to comform with the traditional interpretation of the “life cycle” hypothesis. In particular savings propensities and the elderly dependency ratio would be expected to be negatively correlated. Consumption smoothing over a lifetime suggests that the savings rate should be high when a large proportion of the population are in middle age, with savings being accumulated to finance post-retirement consumption, and then drawn down as the individual ages. But while there is clear evidence of increased saving as the retirement age approaches, the evidence for post-retirement dis-saving is far from clear and even contradictory, suggesting that the bequest motive, or at least the negative utility associated with running down savings may be greater than the original version of the life cycle hypothesis postulated

What the numerical examples and the empirical studies suggest is that it is important to measure pension wealth correctly, since failure to do so can have a major impact on estimates of saving, since mis-measurement of pension income may account for the striking discrepancy between what life cycle models imply about the age/saving relation and estimates of saving rates by age that are derived from looking solely at household data in isolation from information on the value of funds that back pensions. The reason for this is that in the case of those contributing to individually funded pension schemes, wealth dynamics conform a lot more closely to the simple life cycle pattern, since it is steadily built up during the working life and is run down in retirement.

Current Account Implications

That the global economy as it stands is characterised by serious and important imbalances is no longer really a controversial point, since the recent global financial crisis has brought their presence into bold relief. The perception that unsustainable imbalances exist between countries like the US, the UK and Spain on the one hand, and China, Germany and Japan on the other has been widely identified as one of the key forces which lay behind the build up to the recent global economic and financial crisis. But just what dynamic lies behind the creation of these imbalances?

In fact, economists have long recognised that demographic shifts play an important role in determining long-term trends in global capital flows, and hence in global current account balances, and a variety of models have been developed to help explain and understand this important phenomenon. However, since the start of the present century the degree of interest has heightened, and the implications of the ongoing shifts in demographic structure have been highlighted and widely discussed (see, for example, the IMF’s 2004 World Economic outlook or the Boston Federal Reserve Conference in 2001, or the Kansas Federal Reserve’s Jackson Hole Conference in 2005).

Viewed at the most simple and basic level, the current account is literally equal to the ‘net’ saving (total savings minus total investment) that occurs in a given economy over a discrete time period. Given this, a tendency to save more in one economy will be more or less automatically tranformed into a tendency to borrow more in another, since without the presence of a “counterparty” the global books simply would not balance. Increased saving in a given country tends towards the generation of a current account surplus, which in its turn is transformed into an outward flow of capital towards other countries.

Now since, as explained above, savings behaviour generally varies across the age ranges, the relative age structure of a country’s population plays a significant role in explaining the borrowing and lending patterns between that country and the rest of the world. Using models that link demographics, growth and current accounts, a number of economists have attempted to show how demographic shifts have driven global current account trends in recent decades, and tried to determine what conclusions can be drawn about the future evolution of the current balances and imbalances.

One of the key points to grasp, is that the proportion the population which is to be found in one of the ‘prime’ age groups at a given moment in time, is absolutely critical, and much more important for understanding the processes at work than the mere size of the working age population. When we speak of “prime” here, we are talking in terms of prime savers, prime borrowers, and prime productive workers. Where these actual age brackets lie, and the extent to which they may overlap, is still a subject of some controversy, even if the existence of the phenomenon in itself is not in doubt: certain age groups tend to borrow more, others to save more, and worker productivity does not remain constant over the working life, but reaches a peak, and then declines.

Estimates of the exact age extension of the different groups vary, but 25-40 would be a good rule of thumb measure of the borrowing range, 40 to 55 for the peak savers, and 35 to 50 for the prime age workers. Beyond this, the question is an empirical one of measuring and testing to determine more precise boundaries and frontiers.

And the hypothesis being advanced here is that since a country’s credit expansion is driven by the prime borrowing group, the size of this group in relation to the rest of the population is key for determining the overall credit dynamic, and for deciding whether any given nation is going to be a net borrower or a net lender. Looking at the evolution of current account balances from a historical perspective this demographic dimension would appear to have far greater explanatory power than the more traditional “cultural differences” approach.

Obviously the corrolory of the prime borrowers are the prime savers, a group which the IMF defines as lying in the 40 to 65 age range. The share of the developed economy population falling within this bracket is currently increasing rapidly, although it is again important to note that there is great variance across countries in this regard, and while in some cases this population group has already peaked (Germany and Japan) in others (the United Kingdom, France, the United States) it will still not peak for many years to come.

As suggested above, it is Franco Modigliani’s life-cycle theory that provides the most coherent framework for interpreting just how the demographic structure of an economy (how many prime borrowers, how many prime savers, how many children and how many dependent elderly there are) may influence the general desire to save or invest across an entire economy. As also explained above, and by definition, the current account (together with the capital flows that accompany it) is the measure that registers the difference between an economy’s level of savings and investment. When economies are closed to trade and capital flows, savings and investment must be equal and interest rates move up and down to bring these into balance. Traditional monetary and fiscal policy was in fact built on this edifice.

Since the advent of financial globalisation, however, the vast majority of the world’s economies have become relatively open, with funds flowing in and out, with the result that the accumulation of sizeable current account imbalances without sharp short-term shifts in interest rates has become commonplace. So it makes sense that those economies that have younger populations and more “prime borrowers” borrow (on average) from those who have more “prime savers”. And, as a result, it is also plausible that relative demographic profiles can have important effects in determining savings and investment outcomes across countries, and hence the current accounts and capital flows between them. The challenge facing monetary policy in the age of globalisation is to find mechanisms to regulate such flows, since otherwise excessive imbalances accumulate (as we have seen), with economies becoming either excessively export dependent on the one hand, or totally uncompetitive internationally on the other.

And we are steadliy accumulating a large body of evidence which strongly suggests that this is exactly what has been happening. The basic insight that demography matters for the current account, has now been shown to be important in a wide number of studies which have looked at the way in which demographic shifts help to explain changes in growth, savings rates and with them the global economic imbalances .

This formulation of the problem constitutes a great advance, since it has enabled researchers to start to map the impact that having people in particular age groups has on the current account position. Up to a median population age of 40, the demographic structure appears to act as a stimulant for more consumption than can be financed in the short term, and hence acts as a drag on the current account position. As populations age beyond the 40 median age threshold, the credit driven component in consumption tends to decline, and people on average appear to save more than they borrow and spend. Thus the society becomes characterised by a preponderance of so-called ‘prime savers’, with the current account position tending to improve markedly. Hypothetically a further turning point is reached when the steady increase in median age driven by a rise in the elderly dependency ratio means the population once more tends to become a drag on the current account, as a growing number of older people start to spend more than they earn – the so called “dis-saving” phenomenon. To date no society has shown these characteristics, which tends to suggest that people pass more on to the following generations than early versions of the life cycle theory tended to assume, either due to the presence of a bequest motive, or due to uncertainty over the exact length of life. Apart from this empirical observation, it is hard to see what happens to a society in a condition of irreversible ageing as and if their level of national saving turns negative.

This understanding of the prime saving and borrowing phenomenon is important because much of the discussion of demographic issues to date has focused on the size of the working age population (normally defined as those in the age range 15-64) and the evolution in the dependency ratio. Conclusions reached using these two measures differ and the difference can be highly significant. The problem of having a declining working age population can be, to some extent, offset by legislative changes that facilitate higher labour market participation rates, and longer working lives. But there is no such easy answer to the long term decline in the prime borrower group, and this becomes obvious when we look at the frustration which is produced among leaders in Japan and German when G20 meeting talk about the need to set firm figures for permitted current account surpluses.

Demographics and the ‘Savings Glut’

Given this kind of understanding of the demographic component of saving and borrowing patterns it is not hard to see how demographic forces may have played an important role in the run up to the most recent crisis, making possible what Federal Reserve Chairman Ben Bernanke once called the ‘savings glut’. It was this “glut” that lay behind the large volume of cheap liquidity which was available across the planet in the years prior to the outbreak of the financial crisis. Demography may well have contributed to falling global real interest rates as the proportion of ‘prime savers’ in the developed world rose steadily. The global pool of ‘prime savers’ is expected to keep rising, and as a result, the tendency will be for more, rather than less, net saving globally, and the ‘savings glut’ (and lower real rates) may become a more persistent feature of the world than many think.

The notion of the ‘savings glut’, has been a widely debated issue ever since then-Fed Governor Ben Bernanke coined the phrase in a speech on global imbalances in 2005. Evidently, the aggregated global current account balance has to be zero, so if there is a tendency for some of the world’s richest economies to want to save more than they invest (i.e., run a global current account surplus), then the balance can only be resolved by a fall in global real interest rates which produce current account deficits elsewhere. Since this rise in desired global savings was not directly observable, the prima facie evidence was the surge in current account imbalances alongside the presencce of lower real interest rates. This was seen as evidence since the liquidity needed to hold the rates down would only be there in the presence of an significant global savings oversupply. Explanations for why exactly the desire to accumulate savings may have surged vary but since that time the debate has been ongoing about whether the theory is correct and if it will prove fleeting or persistent. The framework for global capital flows and current accounts set out here provides an interesting perspective on this issue.

The Slowdown In Developed World Economic Growth

While demographic changes taking place in the developing countries mean that global growth is currently running at historically unprecedented levels, there can be little doubt that trend growth in some of the older developed economies has been progressively slowing. Trend growth in Italy is now not far above zero, and in Germany and Japan it is only just sustaining the 1% level. This phenomenon will become increasingly important as the number of those in the key 35-54 age group falls relative to those aged over 65 in one country after another. On the global scale the ratio is expected to fall from the current level of 3.25 to 1 to a mere 1.58 in 2050. But the really worrying numbers come from the countries who will have more people aged over 65 years old than between 35-54 by the time we reach 2050. Those in this category are Japan (who fall from a 1.19 ratio to 0.58 over the period), South Korea (a dramatic fall from 3.05 to 0.65), Italy (1.28 to 0.69), Germany (1.19 to 0.69), Spain (1.80 to 0.70), France (1.61 to 0.87) and Canada (2.12 to 0.92). So without significant extensions in working life over the next few years, there will be more retirees than those in their economic prime across large swathes of the Western World as we approach 2050. But even with the increase in working life the productive capacity of the workforce is sure to be affected its the average age rises.

And historical data reveal a relatively good longer-term correlation between risk-asset prices and the proportions of those who are in the 35-54 year age group when compared to those in the child and elderly dependent groups. In principal this age group constitute the main income producers for an economy and their ability to drive activity and invest in assets may well be influenced by the level of economically inactive population they have to support either personally or through taxation. With high and rising rates of economic dependency the burden on the economically active population may become such that consumption is negatively affected while the pool of available money to invest becomes significantly reduced. This implicit ‘productivity ratio’ may well give us one of the best measures available of the likely capacity of the net accumulators of assets in an economy to influence asset prices as the population ages.

In this sense Japan already offers us a clear warning as to what may await the rest of the developed world as a significant part of their population hits the old age dependency stage. In terms of the ‘life cycle hypothesis’ Japan becomes a fascinating test case for what may happen in many countries in the years to come. While it may be statistically difficult to establish whether the bursting of the Nikkei bubble at the end of 1989 and the bursting of the dot.com bubble in 2000 had a common root in changing demographics, it is clear that financial markets have become more prone to bubbles as the pool of potential savers has grown.

Surely it is more than a simple coincidence that the Nikkei peak was hit at exactly the same time as the key 35 to 54 age group arrived at its highest value relative to the dependant groups. That the Nikkei then spent the best part of two decades failing to show any meaningful recovery could also have much to do with the ongoing aging of the population and the decline in the number of those in their economic prime.

Most observers are in agreement that if demography matters then the US will most probably not be the next Japan, although parts of Europe might well be. While the US and Europe have demographic similarities to that Japan has faced for the last two decades, the US does have one key area which could help it escape the fate seen in Japan. This is the simple fact that its population is growing and looks set to continue as far as the eye can see. Japan's population is now falling after broadly stagnating for 20 years. Europe's population has also been stagnating for at least a decade and will continue to do so for the next decade before declining as far as the eye can see, albeit at a slower pace than Japan will continue to do. In contrast the US population continues to grow, with the slowdown in growth quite gentle. A similar picture is seen when we come to the percentage change in the 'economically active' 15-64 year old group. Europe is about to start losing people in this age group as Japan has been doing for the last decade.

So if you accept that having a growing population (especially those in their working age) has formed a key component of growth in many countries in what we have come to call the moden growth era, then it was seem those parts of Europe where labour forces look set to stagnate have a much are much higher risk of an eventual Japan style outcome than the US does.

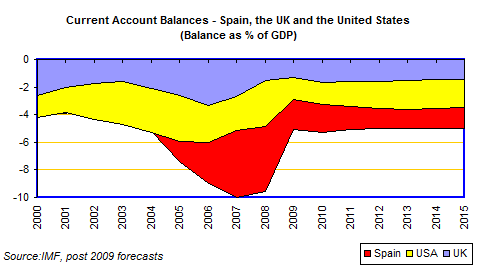

On The Shoulders Of Giants - How Spain Is Destined To Follow In Germany's Footsteps

And nowhere could this situation be clearer than in Spain. The Spanish economy sustained several years of what was clearly above par growth by increasing labour inputs dramatically, while productivity growth remained between low and non exist. In the Spanish case the labour force growth came not from natural population growth, but from labour migration from other parts of the globe, while the demand which supported the growth was also not organic, but fuelled by the very cheap and ample liquidity which had become available with the creation of the Eurowide capital markets. In order to see how this problem may have arisen, and what may now happen to domestic saving in Spain, a comparison between the recent history of the Spanish and German economies can prove illuminating, especially since, as I will argue below, there are strong structural homologues to be observed in the evolution of the two economies, with a time delay of about a decade between the process in one country and that in the other.

The first, rather surprising discovery which an examination of the recent historical data for Germany reveals is that it simply is not true that the Germans are a group of "non consumers", and inveterate savers. Back in the 1990s German private consumption enjoyed a substantial boom, a boom which ground itself to a halt around the year 2000. It is only since 2000 that German private consumption growth has been lacklustre, and seemingly incapable of driving GDP growth. And when we come to Spain, it is immediately evident that Spanish household consumption growth enjoyed a similar expansionary cycle between 1999 and 2007, demonstrating the same kind of "blossoming" (if on a rather larger scale) that German consumption had experienced in the mid 1990s.

More than the phenomenon of the consumption boom in and of itself, what is really important is what it was that was driving it. Unsurprisingly perhaps, what we find when we come to examine the data is that same old "usual suspect" – a very rapid increases in private sector credit. And examined carefully the figures belie the idea that Germans have always been a nation of meticulous savers. The Spanish history of mortgage growth tells a very similar (but even more exaggerated) story to the German one. And, as can be seen, it wasn't only households who were doing the borrowing, corporate entities were rapidly increasing their leveraging too. Interestingly, after years of being almost dormant, corporate borrowing seems to have had a brief renaissance in Germany on the back of the current crisis.

But one more time, when it comes to corporate borrowing the only aspect in which the situation in Spain distinguishes itself is in the magnitude of the phenomenon. Spanish corporate indebtedness has become a much, much bigger issue than German corporate indebtedness ever was. Indeed, while total private sector debt in Germany around the turn of the century was not that different from Spanish private debt today, German GDP at the time was (in relative terms) around twice as large as Spanish GDP is today. And moving forward, if we come to look at the long tail on the stagnation in German year-on-year borrowing, this is the point where we should be able to discern something of the future which awaits Spain, and especially in an environoment where the financial markets have little willingness to finance yet more indebtedness. Interannual lending in Spain simply isn't going to climb back up again towards its previous levels, and we should expect it to trawl around the zero percent mark in the years to come, as Spain's private sector steadily, and somewhat painfully, deleverages itself.

But there is another aspect of the situation which should attract our attention here, and that is the close association between ongoing lending booms and current account balances. Germany was no exception to the general rule here, since all through the duration of its consumption boom the country ran small current account deficits. Deficits which then became surpluses in the wake of the huge structural adjustment the country passed through during the transition from being a consumer-driven to being an export-driven economy.

And this is the path that the Spanish economy will now surely have to follow, even if we should again not miss point that there is a very significant difference in scale between the two cases. In comparison with the process Germany was submitted to between 1999 and 2005 Spain's adjustment will need to be quite literally enormous. As some economists have observed the transition which awaits the Spanish economy is one without precedents, and is certainly right off the map as far as recent historical experience is concerned.

So what is going on here? Certainly the close similarity is too striking to be merely coincidental. The economic literature is replete with examples of countries who experienced financial crises, and then dug themselves out of the hole they found themselves in by increasing their exports (Reinhardt & Rogoff). The reason for this is obvious. Once the private sector in a country gets itself into crisis precipitating excessive debt, there are only two realistic possibilities: restructure the debt, or pay it down. There isn’t a third possibility of getting into even more debt (via for example government fiscal deficit spending), since as we can see at the present time, such attempts have a relatively short life, and the markets rapidly lose patience with this kind of attempt to flee into the future. So given that the restructuring option isn’t an especially attractive one either, most countries ultimately solve their problem, by exporting their way out of difficulty, in order to then restart the credit cycle.

But the conjecture advanced here goes beyond this, since what is being postulated is not the idea of economies which are temporarily export driven, but of ones which become completely export dependent.

The argument than now follows is more of a hypothesis than anything else, but if we look seriously at all the above argumentation above about how demographic processes affect patterns of national saving and borrowing, and if we accept that ageing is (whatever the drivers of fertility declines may be), as a matter of fact, an irreversible process, and if we pay careful attention to the recent historical experience of countries as they age, then it does seem not unreasonable to postulate that there is a transition which occurs, and that this transition has at its centre a steady transformation of the current account balance.

As we have seen, it economies transit from being consumption driven to export driven, and it would appear that the process is not merely random, a question of options or “growth models”. There is not a choice here, since there are deep underlying structural dynamics at work, and these dynamics seems to be intimately associated with the dynamics of the demographic transition. As I am trying to argue in the German case, the shift doesn't seem to be a cultural one, or a pure question of public policy. And the hypothesis is empirically testable, in the sense that if Spain does follow Germany down the exactly the same road then this will count as additional corroboration for the thesis.

But what could be really be driving this transition? Well, as the young Danish economist Claus Vistesen and I have suggested on a number of occasions, the close association of the export dependent phenomenon with population ageing and the demographic transition which lies behind it may well provide us with the key. Using Modigliani's life cycle saving and borrowing idea, and the Swedish demographer Bo Malmberg's idea of population "ages" (child, young adult, middle aged and elderly), Claus Vistesen has prepared the adjacent chart which attempt to illustrate the process which might be at work.

The current account balance is here associated with dependence, or lack of it, on exports. Very young societes, such as those which are to be found in the African Sahel, or Uganda, or Pakistan, or Bolivia, have very low saving rates due to the high preponderance of those under the working age, and as a result are dependent on current account deficits and imports to maintain a minimum standard of living for all. If markets were completely rational in this context, they would be prepared to finance these deficits conditional on policies to reduce fertility and raise female empowerment, which are sure ways to reduce the level of child dependence, in the same way they are prepared to finance elderly but highly indebted European societies conditional on policies to raise labour force participation rates and extend the working life via reform of the pension systems.

At the other extreme, elderly societies become increasingly dependent on exports to avoid falling into dis-saving, and negative current account balances, since the once the current account balance deteriorates into negative territory it is unclear how the situation can ever correct itself, given the absence of homeostatic processes.

Of course, all of the above remains for the time being at the level of hypothesis. What is beyond doubt is that Spain’s boom bust cycle followed Germany’s by a decade, while their demographic profile also reveals a ten year lag between one country and the other. In term s of median population ages Spain is roughly at the same point today as Germany was at the turn of the century. And when we come to the percentage of the 25 to 40 age group in the total population, we can see that this peaked in Germany at the end of the 1990s, while it is peaking in Spain at the present time.

A Delicate Balancing Act

Returning to the issues raised at the start of this chapter, three major issues arise from this demographic perspective on capital flows and current accounts. First, we have significant empirical confirmation that the recent global imbalances were, in part, offshoots of slow-moving underlying demographic determinants of global capital flows. While some progress has been made towards reducing them (and in particular in the US), there is still a long way to go. In particular further adjustments in global demand and currency patterns are still needed, and in particular more contribution is needed from China.

Second, while the near-term adjustments will mean more emerging market deficits and less developed market ones DM deficits.

Third, at a global level, demographic pressures will continue to imply that the increase in desired saving will exceed the increase in desired investment. This has one clear implication: globally interest rates can be expected to remain low. As argued in the “savings glut” thesis, population ageing in the developed world may have been more important in pushing real interest rates down globally over the last 10-15 years than is often acknowledged. This process surely has still more to run and real interest rates may stay low for longer than many currently expect. Those who worry that the ageing of developed markets may put upward pressure on their interest rates and downward pressure on their asset markets in the short term may prove to be underestimating the safety valve which global demographic processes will offer. Taking these forces together, it seems likely that significant net flows of capital across border are likely to remain a feature of the landscape and may be set to grow further. This means that developing the infrastructure, policy tools and regulatory settings to be able to cope with them is likely to remain an urgent task.

On the other hand, looking at the savings, investment and capital flows story exclusively from the perspective of the large developed markets may end up being misleading in a world where the global picture is increasingly changing. Crossborder capital flows are likely to remain significant given that the impending demographic shifts may increase rather than diminish them. Efforts to improve the quality of global financial regulation and the monitoring of cross-border capital movement may assume an added importance, as will the coordination of monetary policy, and agreements on currencies at the G20 level. The lessons of the recent crisis suggest a particular need to ensuring that the financial markets in the developing countries can cope with substantial capital inflows without producing a serious misallocation of resources and structural distortions in the receiving economies. In particual a deepening of capital markets in some key Emerging Markets may well reduce some of the excessive pressure to ‘export’ savings.

In terms of policies to address the pressures of ‘ageing’, the debate in terms of social security and healthcare often focuses on raising retirement ages to reduce dependency rates and alleviate fiscal pressures. The impact of those kinds of shifts on net savings is a little less transparent, since the shift to private savings patterns at different points in the life cycle in response to a higher retirement age are less obvious than the impact on incomes, retirement payments and tax receipts. However, the fact that demographic pressures seem to be currently pushing most developed economies towards larger current account surpluses is arguably indicative that these countries are unlikely to become significant “dis-savers” in the near future.

Extending working lives relative to the time spent in retirement will not only help address the pension issue, it should also serve to accelerate the tendency towards larger current account surpluses accross most developed economies, in particular in those parts of Europe which are in the process of private sector deleveraging as part of their fiscal sustainability programme. What this willl effectively do is raise the upper bound on the ‘prime saving’ age and extend the threatened “dis-saving” era well out into the future.

Running behind such shifts are not just the changes in the prime saving and borrowing populations as between developed and developing markets, but also changes in relative economic size and importance of the economies in the two groups, as withnessed by the recent rapid rise of countries like China and India. This process carries with it the implication that the relative weight of the two groups in the global economy will change sharply over the coming years with the result that GDP in the devloping world will rise significantly, from around the current level of 33% of global GDP to something like 70% by the time we reach 2050.

This is what makes it theoretically possible for both developed economy surpluses to rise and emerging market deficits to deteriorate (as percentages of GDP) at one and the same time. Since the Emerging Market share of GDP is rising, relatively modest deficits are all that will be needed to offset the large developed market surpluses which will be produced. And as is being stressed here, shifts in the relative proportions between the various ‘prime age’ population groups are not identical to the shifts in the share of the working age population in terms of their timing and their potential impact, although the two are clearly related. The working population issue is much better known and has been important in defining acceptable levels of fiscal liabilities as well as a whole battery of structural policy issues. But the general profile in terms of the varios peaks in the prime goups is different to the profile suggested by the peaks in working age population shares, and since it is common practice to use these latter in order to estimate the evolution of the current account (see, for example, the IMF 2004 World Economic Outlook study of the problem), such distinctions are potentially important and hence a more detailed empirically grounded study of impacts of these demographic changes in all their complexity is an urgent necessity.

What Are The Risks Of A Meltdown In Housing and Equity Markets?

Given the relative distributions of wealth and income between countries, it is evident that the rapidly ageing developed economies currently account for the overwhelming majority of global investable assets. And as we have seen, basic life cycle theory suggests that as the large baby boom generation cohorts slow their saving rate (and eventually even draw down on their savings) the steady retirement of this generation can have a significant impact on asset prices, effectively driving them down. The big question is, of course, to what extent. Will ageing lead to a global asset price meltdown? The current consensus (see Poterba, 2004) is that while ageing will undoubtedly have a significant negative impact on asset prices, an asset price meltdown of the kind some have predicted (see Mankiw and Weil, 1989), is unlikely.

But saying there will not be a meltdown is not the same as saying that there will be no impact. In a recent study of ageing and asset returns (From The Golden To The Grey Age) Deutsche Bank analysts Jim Reid and Nick Burns argue that the ‘Golden Era’ for equity returns seen between the early 1980s and mid-2000s was at least in part demographically led, and is unlikely to be repeated. Instead, the authors argue, what we are likely to see is more volatility in stock values, shorter business cycles, significant quantities of liquidity, and sub-average returns in many asset prices.

However, even if most of the attention has so far focused on values in equity markets, the impact of changing demography on house prices is likely to be equally (if not more) important. Demographic factors have clearly contributed to real house prices increases in many countries in recent decades, even to the extent of producing housing bubbles in some. For instance, favourable demographic changes are estimated to have added an additional 80 basis points per annum to United States property values over the past forty years as compared with what would have happened with neutral demographics. On the other hand the looming negative demographic impact which awaits the US over the next forty years has an estimated value of around 80 basis points per annum. And as we have been arguing, the position in Europe and Japan is expected to be even worse. In fact Japan seems to have been the pioneer in this case, and property and land prices are still well below their peak 1992 values. And given the existence of a negative wealth effect, the impact of changes in property values on global asset prices could also be significant.

Both the lifecycle and the overlapping-generation models of saving and borrowing are based on the simple idea that the young save for old age by buying assets, while the old sell assets to finance retirement. The asset transfers involved can occur directly or involve the intermediation of institutions such as pension funds, but regardless of the details, the change in the relative size of the asset-buyer group and asset seller one has clear consequences for future asset prices.

In particular, the asset purchases of a large and wealthy generation, such as the United States baby boomers, passing through the prime saving age range, evidently drives asset prices up well beyond a demographically neutral mean. Conversely, as a country’s population ages, generations become relatively smaller, causing asset prices to decline below their demographically neutral historic mean. Stylized ageing and asset price trends in countries like the United States and Japan seem to support the theoretical conclusions that can be drawn from these kinds of model. In the 30 years leading up to the financial crisis, during the prime economically active years of the baby boomer generation, US asset prices rose substantially. Ex-ante real interest rates fell, equity P/E ratios increased and the real level of house prices climbed. Standard theory then seems to suggest that asset prices propelled by the boomers’ savings will be come under continuing pressure as this large generation retires and starts to sell its assets to the relatively smaller generations that follow. Coincidentally or otherwise, the start of this boomer retirement process occured at precisely the same moment as a major drop in US house prices took place.

Empirical studies examining the correlations between ageing and asset prices basically fall into two main groups: single country investigations of financial asset and house prices, and international studies of financial asset prices.

In the case of single country studies, identifying the impact of ageing on asset prices is difficult, because ageing progresses at a comparatively slow rate and there is no clear consensus on how best to measure population ageing. Although ageing can be viewed at the present time as primarily a developed country phenomenon, as we have seen the differences between the rate of ageing in one country and another may be highly significant.

Also, the focus of the studies that have been carried out have varied. Some have looked at a variety of age cohorts: Mankiw and Weil (1989) and Hendershott (1991) focused on adult populations; Yoo (1994) and Bergantino (1998) examined a number of age cohorts in detail; while Poterba (2004) studied prime savers (who he considered to be individuals between 45-60 years of age). Others, for instance, Bakshi and Chen (1994), used average age. These different measures make it very easy, as Brooks (2006) argues, to make the casual and econometric link between ageing and asset prices in a single country study. However, this implies that the causal identification established could be questionable. For instance, Engelhardt and Poterba (1991) showed that the demographic factors identified in Mankiw and Weil (1989) for the United States do not fit Canadian house price and demographic data. International studies can improve on single country studies as they offer the possibility of investigating several ageing trends simultaneously. Davis and Lee (2003) found, for example, that prime saving cohort size is significantly correlated with asset prices in a seven country sample. Brooks (2006) also extended sample size to include more countries and ageing trends. International studies are also useful to revisit single country results. Ang and Maddaloni (2005) found, for instance, that average age does not predict real returns outside the United States.

However, even international studies using financial asset price data present difficulties, because capital mobility is expected to dilute the impact of ageing. If ageing affects asset prices, investors living in ageing (ie low-return) economies should move their assets to more youthful (ie high-return) economies until expected returns equalize. Indeed, Higgins (1998) and a long line of subsequent studies show that this is exactly what is happening: capital flows from ageing economies to relatively younger ones. Thus, the presence of capital flows make it even harder to identify the precise impact of ageing on financial asset prices.

In principle house prices might be considered to offer better identification criteria than financial asset prices as capital flows are less likely to dilute the link between ageing and asset prices. Cross-border investment in residential housing is more complicated and consequently less common than cross-border financial investment. Hence, using real house price data collected by the Bank for International Settlements (BIS) covering 22 advanced economies between 1970 and 2009 Elod Takáts (Takáts, 2010) found there was sufficient heterogeneity in both house prices and demographics to offer a solid basis for isolating and identifying the impact of ageing. Unsurprisingly the model found that a combination of real economic factors and demographic ones drive asset prices.

Thus a one percent increase in real GDP per capita roughly corresponded to a one percent increase in real house prices. Similarly, a one percent increase in population implies was associated with a one percent rise in real house prices, while a one percent increase in the dependency ratio lead to a drop in real house prices of two thirds of a percentage point. The differing demographic impacts on real house prices aross countries was a reflection of variations in the rhythm of the ageing process. For instance, while in the United States, the model estimated that favourable demographics added around 80 basis points per annum to house prices between 1970 and 2009, in faster ageing countries, such as Germany or Japan, the demographic impact was already found to be negative.

Extending the model to a broader group of countries, and using the UN (2008) population, the author carried out projections in an attempt to estimate the future impact of ageing on real house prices. Unsusprisingly he found that house prices will face substantial headwinds over the next 40 years. Ageing will decrease United States real house prices by around 80 basis points per annum compared to neutral demographics, while the effect was found to be much stronger in both Europe and Japan. However, even though the impacts are somewhat larger than those to be found in most of the prior literature, the estimates are still short of the Mankiw and Weil’s (1989) asset price meltdown projection, which suggested around 300 basis points per annum real house price decline.

Whatever the empirical fine tuning we will see in the future, it is clear that house prices in the developed world are going to suffer a negative demographic impact in the years to come . In addition, since movements in house prices are normally a close correlate with movemements in financial asset prices, if house prices face headwinds, then so should financial asset prices. Using estimated coefficients and global population forecasts, Elod Takats found that asset prices would face headwinds up to a full percentage point. This impact is substantial, but based on historical returns would not necessarily imply real asset price declines. Furthermore, even if ageing continues as expected currently expected, a variety of other factors can interven which affect the relationship between demographics and asset prices. These uncertainties along with the magnitude of ageing related asset prices changes suggest that more research is needed before too many conclusions regarding public policy are drawn.

And The Dangers of Sovereign Debt Default?

Lastly we have the impact of population ageing on Sovereign Debt. One of the most striking features about the difficulty many economies are experiencing in exiting the current crisis, is the degree of sensitivity of the financial markets to negative dynamics in the sovereign debt of countries which were classified as AAA as they entered the crisis. This sensitivity is hard to understand if the difficulty were only one of resolving the immediate difficulties created by the crisis. What seems to be happening is that two crises are merging, the one we are in the process of leaving behind, and the one which lies out there in front: the sustainability of welfare commitments in the face of rapidly changing population pyramids.

According to a recent report from Standard & Poor's Ratings Services (Standar & Poor’s, 2010), the cost of caring for the growing numbers of dependent elderly will both affect growth prospects and dominate public finance policy debates across the globe, and for many years to come. Even if most governments have long been aware of the need to prepare for the looming problem, the rapid build-up of government debt over the past three years has effectively heightened the need to do more to advance reforms aimed at containing the risks to sovereign budgets, especially in countries with high expected future increases in age-related spending. Currently, relatively high general government deficits are complicating efforts to rapidly improve public finances, particularly in a number of advanced economies and this will surely lead to further debt accumulation over the medium term, even, in extreme cases producing the need for debt restructuring

In principle, during the next decade many governments were expected to have some breathing space given the relatively moderate pressure from age-related spending that was anticpated over the period. However, as S&P’s point out, while this window for implementing fiscal sustainability strategies still remains open, the need to make changes is becoming urgent in the face of the expected strong acceleration in spending which will start in 2020. Against the backdrop of large deficits in some countries, the process of carrying out budgetary consolidation and pension or health-care system reforms simultaneously will prove politically challenging in the countries which are furthest behin in their reform agendas.

As indicated above, population ageing will lead to profound changes in economic growth prospects for countries in the developed world, at the same time as the most affected countries will experience heightened budgetary pressures from greater age-related spending needs. In the absence of appropriate budgetary adjustment, additional reforms to pension and health-care systems, or structural measures to improve growth potential, the future fiscal burden will increase significantly across the board. This burden will not fall equally, though, since the deterioration in public finances over the period 2010-2030 is expected to be particularly significant in Japan, Germany and most of Southern and Eastern Europe. The relevant characteristics of this group of countries is the presence of a relatively high level of existing social security coverage combined with a rapid worsening in the demographic profile.

And the numbers are preoccupying. Assuming no policy change Standard and Poor’s estimate that developed country deficits could rise from 5.7% of GDP currently to over 7.4% of GDP by the mid-2020s. The interest cost of the growing debt burden may exacerbate the budgetary impact of demographic spending pressure. And if nothing is done deficits will rise inexorably to 10.1% of GDP in 2030 and 24.5% by the middle of the century. This would lead the general government net debt burden to increase to 78% of GDP through to 2020, only to then accelerate thereafter. By 2030, the net debt burden is projected to be at almost 115%, at the same time as being on an explosive path to which would see average developed country sovereigns hitting 329% of GDP by 2050. And under such a scenario the economic size of the state would increase significantly with government spending rising to almost 68% of GDP in 2050, up from 46.7% today.

Of course, such numbers are not either fundable or sustainable. They are only a simple illustration of what would happen if changes are not made. Clearly the main driver of the projected deterioration is the long-term increase in age-related spending, which only serves to underline the importance of addressing the projected increases in ageing costs. Simply having the objective of attaining a balanced budget by 2016 would contribute significantly to reducing the overall future budgetary burden, although the strongest pressure on government budgets is expected in those sovereigns where reforms to pay-as-you-go (PAYGO) pension systems are still pending.

In the face of rapid shifts to their demographic profiles, governments in a number of countries (Spain and Slovenia, for example) are currently preparing reforms to their PAYGO pension systems, reforms which are likely to include raising the statutory retirement age, changes to pension indexation formulas, and other measures, while in other (like South Korea and Slovakia, where demographic profiles appear to be the most unfavorable) future increases in pensions have already been cushioned to some extent by earlier systemic reforms.

Evidently, emerging market sovereigns are in general in a relatively better position due to their current level of economic development and their relatively lower pension system coverage. With a few exceptions, these sovereigns are characterized by significantly lower median pension spending to GDP (6.4%) than advanced economies (9.2%). Nevertheless, risks do exist for future pension spending even in this better case scenario. In particular, given that these countries currently have quite young populations, their old-age dependency ratios will eventually deteriorate even faster than they will in a typical advanced economy, albeit even by the time we reach 2050 they are still expected to have relatively lower old-age dependency ratios than the advanced economies. It is important to note that long-term pension projections for Emerging Market countries are based on the assumption that the policy coverage and adequacy don't change. Any broadening of the coverage of the pension system in the future is not incorporated in the current projections, and it is not unreasonable to assume that as these economies develop, government welfare spending may grow faster than GDP as has been the trend in advanced economies during the last half of the 20th century. Clearly, in this case, the current projections are likely to be optimistic.

Conclusions

As we have seen, the challenge represented by the current wave of demographic changes is almost without historic precedent. Large changes in fertility and life expectancy have occured in the past (at the time of the industrial revolution, for example), but these have almost always had positive impacts on the workforce and on economic growth potential. No we are enetering an epoch when the opposite will be the case, and demographic processes will work to slow growth, and to make it more difficult to sustain the standards of life to which we have become accustomed.

The coming decade will be a challenging one for public policy in Spain. Not only have the consequences of the earlier crisis still to be fully addressed, but preparations have to be made for the one which is to come. The recent proposed reforms of the pension system should be seen in this light, as a measure which has more to do with difficulties which are to come then with concrete steps to emerge from the long recession. And as we have seen, in the years to come the whole structure of Spanish economic life is facing a massive transformation. It is not only a question of plugging a gap left by the decline in the construction industry. What is involved is a whole change of mindset, from being a nation of borrowers to one of savers, and it is important that those who manage the nations financial institutions are aware of what this change is, and why it is taking place.

Bibliography

Allais, Maurice (1947) Economie et interet, Paris: Impremiere Nationale

Ang, Andrew and Angela Maddaloni (2005) - Do Demographic Changes Affect Risk Premiums? Evidence from International Data, Journal of Business, 78, 341-380.

Bakshi, Gurdip S., and Zhiwu Chen (1994) Baby Boom, Population Ageing, and Capital Markets, Journal of Business, 67, 2, 165-202.

Batini, Nicoletta, Tim Callen, and Warwick McKibbin (2006) - The Global Impact of Demographic Change, IMF Working Paper 06/09

Bergantino, Steven (1998) - Lifecycle investment behavior, demographics, and asset prices, Doctoral Dissertation, MIT

Börsch-Supan, Axel H; Alexander, Ludwig; and Krüger Dirk (2007) – Demographic Change, Relative Factor Prices, International Capital Flows and their Differential Effects on the Welfare of Generations, NBER Working Paper No W13185

Brooks, Robin J. (2006) - Demographic Change and Asset Prices, in Demography and Financial Markets, Reserve Bank of Australia

Bryant, Ralph C (2004) – Cross-Border Macroeconomic Implications of Demographic Change, Brookings Institute Working Paper

Bryant, Ralph C (2006) – Asymmetric Demography and Macroeconomic Interactions Across National Borders, Brookings Institute, the paper was presented at a conference hosted by the Reserve Bank of Australia

Diamond, Peter A. (1965) – National Debt in a Neoclassical Growth Model, American Economic Review, 55, 1126–1150

Davis E P and C Li (2003) - Demographics and Financial Asset Prices in the Major Industrial Economies, Brunel University Public Discussion Paper No 03-07.

Feldstein, Martin and Horioka (1979) – Domestic Saving and International Capital Flows, NBER, working paper no. 310

Gómez, Rafael & Hérnandez de Cos, Pablo (2006) – The Importance of Being Mature, The Effect of Demographic Maturation of Global Per-Capita GDP, ECB Working Paper no. 670 August 2006

Hendershott, Patric H. (1991) - Are real house prices likely to decline by 47 percent?, Regional Science and Urban Economics, 21 (December), 553-565.

Henriksen, Esben (2002) – A Demographic Explanation of U.S. and Japanese Current Account Behavior, Graduate School of Industrial Administration, Carnegie Mellon University

Higgins, Matthew (1998) – Demography, National Savings, and International Capital Flows, International Economic Review, Volume 39, pp 343-69

Lürhmann, Melanie (2003) – Demographic Change, Foresight and International Capital Flows, MEA discussion paper series 03038, Mannheim Research Institute for the Economics of Aging (MEA), University of Mannheim

Malmberg, Bo and Lindh, Thomas (1999) – Age Distributions and the Current Account A Changing Relation? Working paper series 1999:21, Uppsala University, Department of Economics

Mankiw, Greg., and Weil, D. N. (1989) - The Baby Boom, the Baby Bust and the Housing Market, Regional Science and Urban Economics 19: 235-258.

Modigliani, Franco & Ando, Albert (1963) – The “Life Cycle” Hypothesis of Saving: Aggregate Implications and Tests, The American Economic Review, vol. 53, no. 1, part 1 (Mar., 1963) pp. 55-84.

Modigliani, Franco and R. Brumberg, (1954) – Utility analysis and the consumption function: an interpretation of cross-section data, in Kurihara, K., (ed.) Post-Keynesian Economics, Rutgers UP, New Brunswick, NJ, 388-436

Poterba, James M. (2004) - Impact of Population Ageing on Financial Markets in Developed Countries, Federal Reserve Bank of Kansas City Economic Review, 89(4), pp 43–53.

Reid, Jim and Burns, Nick (2010) – From The Golden To The Grey Age, Deutsche Bank special report.

Samuelson, Paul A. (1958) – An exact consumption loan model of interest with or without the social contrivance of money, Journal of Political Economy, 66, 467–482.

Standard & Poors’s (2010) – Global Aging 2010, An Irreversible Truth

Takáts, Elod (2010) – Ageing and Asset Prices, Bank for International Settlements, Working Paper No 318

Yoo, P. S. (1994) - Age Distributions and Returns to Financial Assets, Federal Reserve Bank of St. Louis Working Paper 94-002B.